Introduction

In Part 1, we traced insurance's evolution from ancient merchants through cyber coverage. Now let's examine who's actually protecting digital assets today.

The market has three main segments: traditional insurers adapting old models, crypto-native solutions building new ones, and tech providers bridging the gap. Each approaches digital asset risk differently. Understanding these differences - and the gaps between them - is crucial for institutions entering the space.

This article maps today's landscape: the providers, what they cover, and how they assess risk. You'll learn:

- Who the key players are in each market segment

- What coverage types actually exist

- How providers evaluate and price risk

- What a typical day looks like for an underwriter

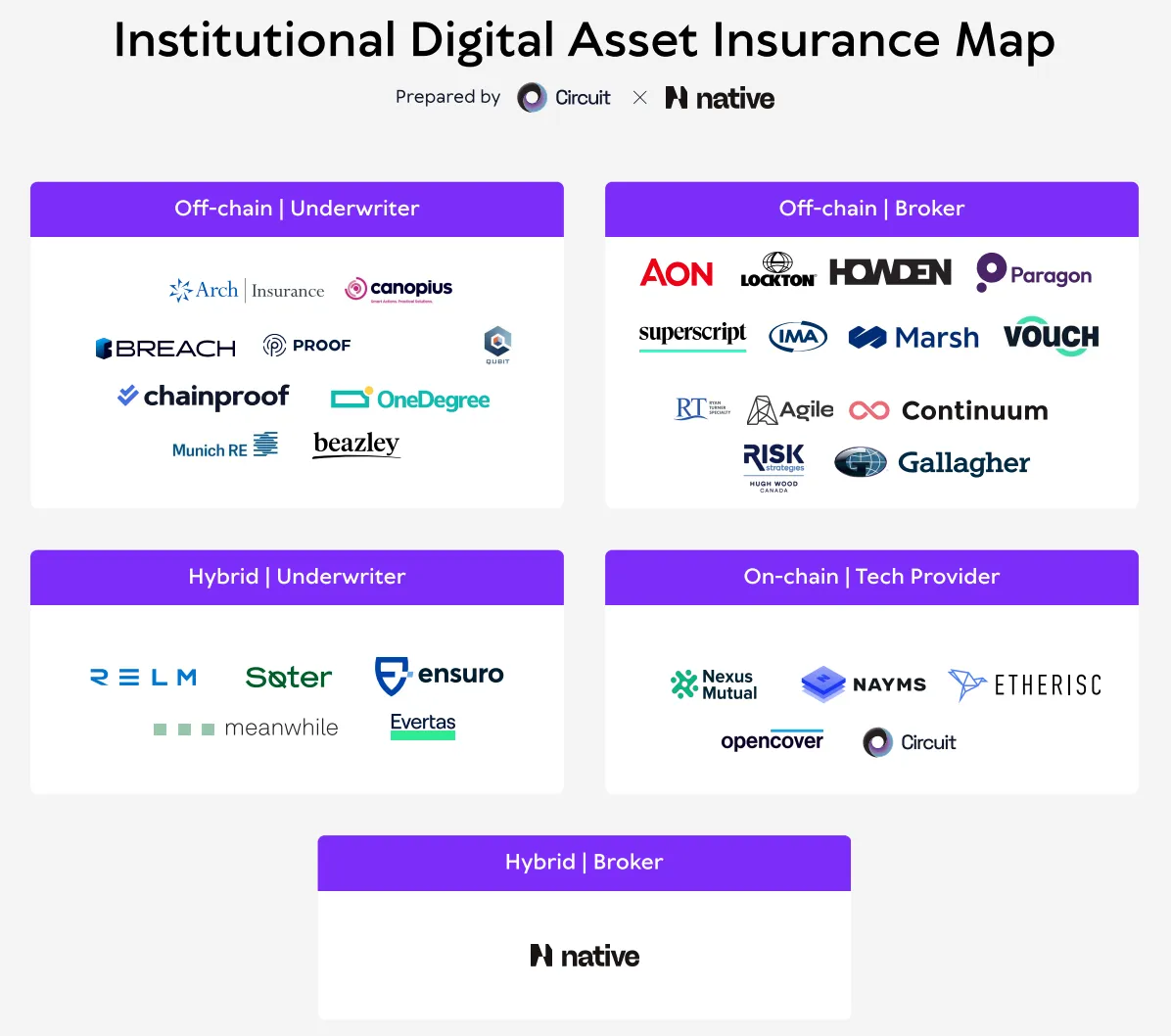

The Players

Insurance involves two roles, regardless of asset type:

- Underwriters: assess risks and provide capital to cover them. They determine what risks they'll accept, set premiums, and pay claims when losses occur. Most people think that insurance companies make money from insurance, whereas they actually make a large portion of their money from investments. Insurers are measured on loss ratios which are the difference between the premium paid to them and claims paid out. Most insurers want to run a sub-90% combined loss ratio, which includes claims payments, broker commissions and operational expenditure. In this scenario, the insurer would make 10% profit for the year of account. In bad years, carriers can run 120% or even 200% in combined loss ratios which would mean for every $1 they took in they paid out $2.

- Brokers: connect clients with underwriters. They understand client needs, find appropriate coverage, and help structure solutions. Think of them as insurance matchmakers. Brokers make money by taking a commission from every account they place with insurance companies. The premium that is quoted to the end client incorporates the commission that the insurance company pays, this generally ranges from 15%- 35%. Brokers can also be remunerated by something called Contingent Profit Commission (CPCs) which is payable by the carrier to the broker for writing profitable business. In this model, insurers pay the broker a bonus for business that doesn’t have a claim with the carrier over a period of time. This CPC can be very lucrative for brokers and incentivises them to place a large amount of low risk business with carriers that offer this structure.

Digital Asset Structure

In digital assets, this traditional structure has evolved into three categories:

- Traditional Players: Established insurers and brokers adapting their models to digital assets. They bring deep capacity but often limit coverage to familiar risks like cold storage.

- Underwriters: Lloyd's syndicates lead specie coverage, focusing on cold storage where risks mirror traditional custody. Major carriers like Arch and Canopius provide significant capacity but maintain strict risk controls.

- Brokers: Marsh, Aon and other global brokers leverage institutional relationships to arrange coverage. They excel at larger multinational programs but often lack deep crypto expertise, agility and technology integrations.

- Crypto-Native Solutions: New providers built specifically for digital asset risks. They understand technical complexities but typically lack the financial strength rating or the brand power that the established insurance companies have..

- Underwriters: Focus on technical risks traditional insurers avoid - smart contracts, D&O liability, hot wallets, mining operations. Underwriters like Relm, Evertas and Soter have emerged over the past few years to take on risks that traditional underwriters haven’t been ready to assess.

- Brokers: Specialized firms combining insurance, onchain capabilities and crypto expertise. These firms help structure coverage for novel risks and navigate technical requirements in both the traditional insurance market and the onchain one. Native is a new broker that combines their broking experience and relationships with onchain capital and capabilities.

- Marketplaces: Crypto native companies grew tired of traditional insurance recognising and responding to novel risks in the DeFi space, so they went out and built their own. The largest and best known of these companies is Nexus Mutual. Risks tend to revolve around smart contract hacking and slashing.

- Tech Providers: Build tools both sides need to make digital assets insurable at scale - from risk monitoring, to marketplace infrastructure, to claims verification. Circuit is a tech company that provides keyless recovery services to ensure companies never lose access to their private keys, this in turn improves the risk profile and allows companies to get a discount on their insurance or help make them insurable in the first place.

Current Market State

Today's market remains heavily skewed toward traditional players, but also remains fractured. Most capacity sits with established insurers and brokers, focusing mainly on cold storage risks they understand well. However most insurers are certain they have the correct wording and risk framework over their competitors. This has led to some markets preferring to not work with others who have different wordings, ratings or underwriting rationale than them. Acknowledging the nascent nature of crypto along with the promise of growth in the space, each player is keen to protect their competitive advantage which can sometimes mean not collaborating or sharing risk with each other, which comes at the disadvantage of the client.

Crypto-native solutions (specifically onchain insurance solutions for smart contract hacks and slashing), while growing, represent a small fraction of available coverage. This imbalance creates challenges - traditional players hesitate on technical risks, while crypto-native providers lack the financial strength rating and capacity major institutions need for contracts or their own risk management appetite.

Even with the fractured state of the market, there has never been more insurance companies writing digital asset risk. With the maturation of the digital asset industry, new insurers are starting to take notice and write policy wordings that they’re familiar with.

Types of Coverage

Specie Insurance is like a high-tech version of traditional vault insurance, specifically designed for cryptocurrency cold storage. Think of it as protecting crypto assets when they're stored offline in secure facilities. It kicks in if private keys or hardware devices are physically stolen, and importantly, it also protects against insider threats - like if employees or authorized signers try to collude to steal assets.

Hot Wallet Coverage is essential for any crypto business keeping assets in internet-connected wallets. It's similar to having insurance for an online bank account, protecting against various digital threats. Whether it's hackers breaking in, dishonest employees stealing funds, or simply human mistakes in operations, this coverage helps manage those risks.

Smart Contract Coverage is particularly interesting because it protects against the unique risks of blockchain technology itself. If there's a flaw in the code that powers a blockchain application, or if someone finds a way to exploit the economic mechanics of a protocol, or if the protocol itself fails in some way, this insurance helps recover those losses.

Miner Insurance is more traditional in nature - it's essentially business insurance for crypto mining operations. It covers physical damage to mining equipment which is crucial given the significant investment in mining hardware and facilities.

Insured Wallets represent an innovative approach to crypto security. Rather than just compensating for losses, these solutions actively help recover access to digital assets if private keys are lost or if the wallet provider fails. It's like having both insurance and a backup system in one.

Directors & Officers (D&O) insurance is vital for anyone in leadership positions at crypto companies. Running a digital asset company involves making complex decisions in a rapidly evolving space. This coverage protects executives if their business decisions result in legal challenges or claims against them personally.

Errors & Omissions (E&O) insurance protects crypto businesses that provide services to clients. If a custody service accidentally loses client funds, or if a trading platform makes a serious mistake that costs clients money, this insurance helps cover those losses.

Risk Assessment Framework

Risk assessment frameworks change depending on what type of coverage a company is looking for, however, we posit that there is more interconnection between risk factors than historical underwriting takes into account. As a starting point, let’s go through what underwriters take into account when underwriting some of the above products:

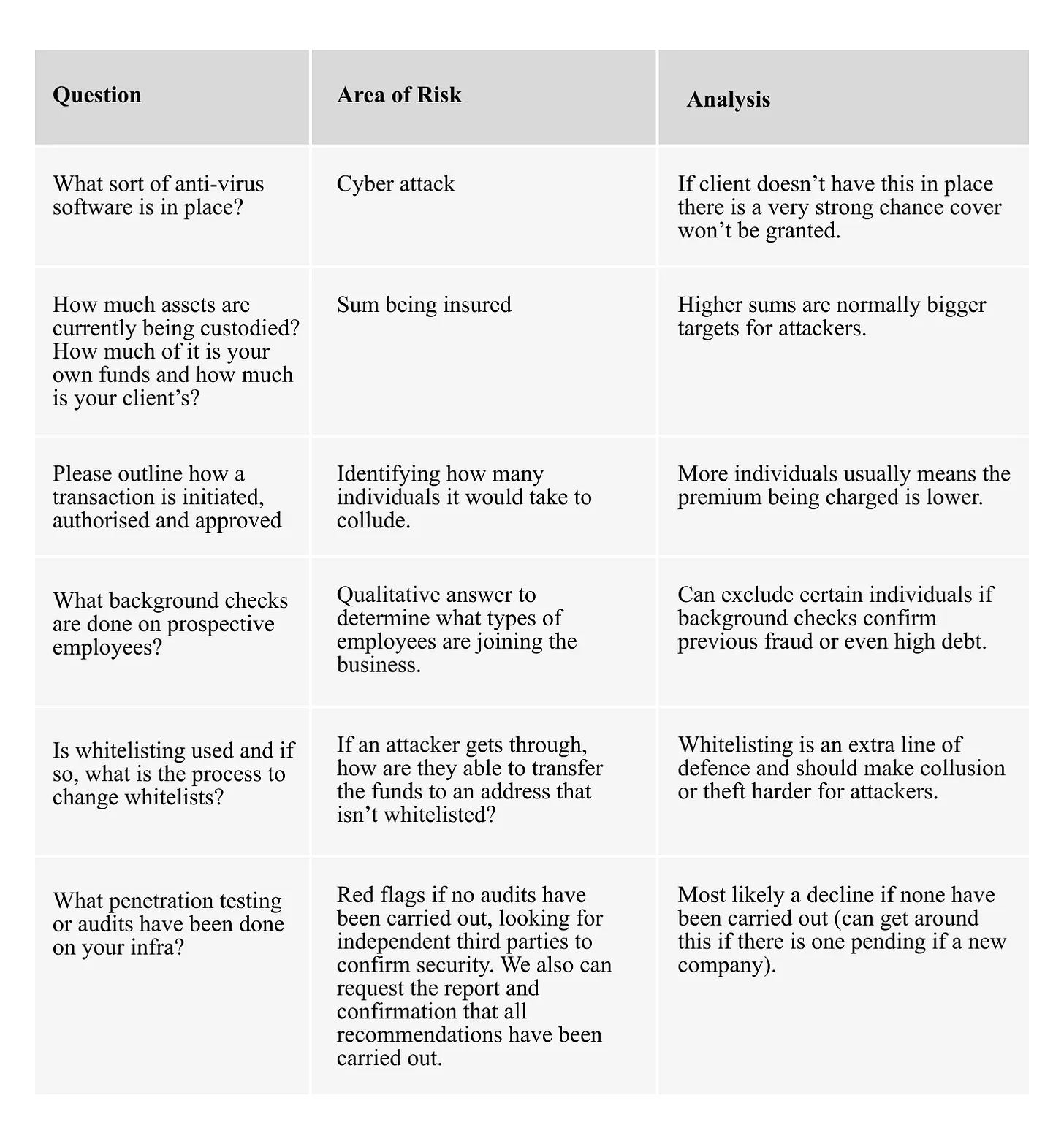

Hot Wallet Coverage:

As hot wallet coverage protects the clients against crime attacks (mostly cyber attacks and social engineering) underwriting this risk comes down to the cyber security the company has in place. This is also coupled with how the client is safeguarding their private keys and how a transaction can be authorised. There is also underwriting around the types of people that are working at the company, even going so far as to understand how background checks are done and who has ultimate authority when things go wrong.

Here is a non-exhaustive look at what underwriting questions could be asked when assessing Hot Wallet risk:

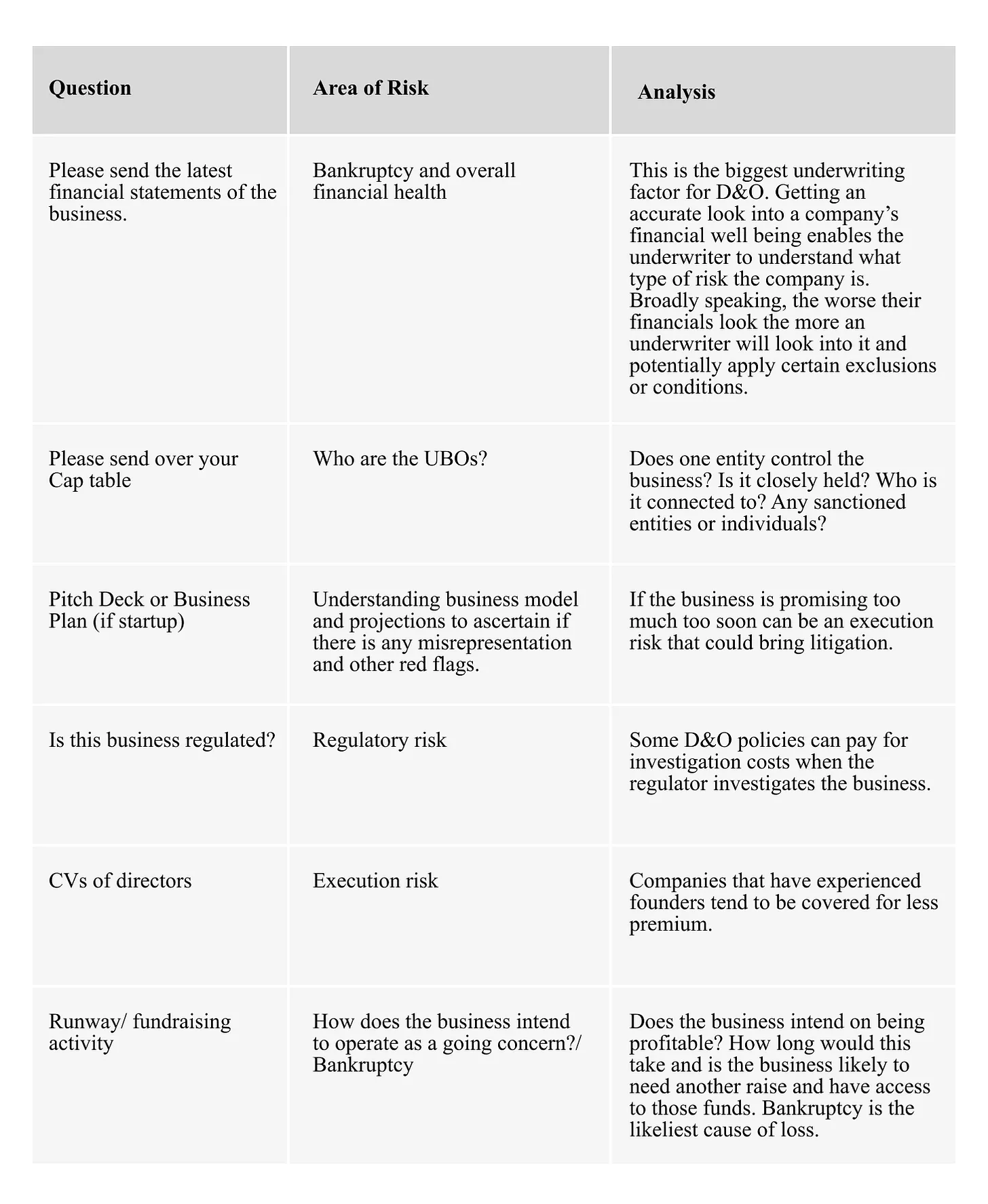

Directors and Officers Liability (D&O) insurance

D&O is the most commonly sought after policy that a company can take out when operating in the digital asset space. Unlike the other policies in this list, D&O policies pay out on behalf of the personal assets of the directors which means it provides an important layer of protection for directors of the company.

Here is a non-exhaustive look at what underwriting questions could be asked when assessing D&O risk:

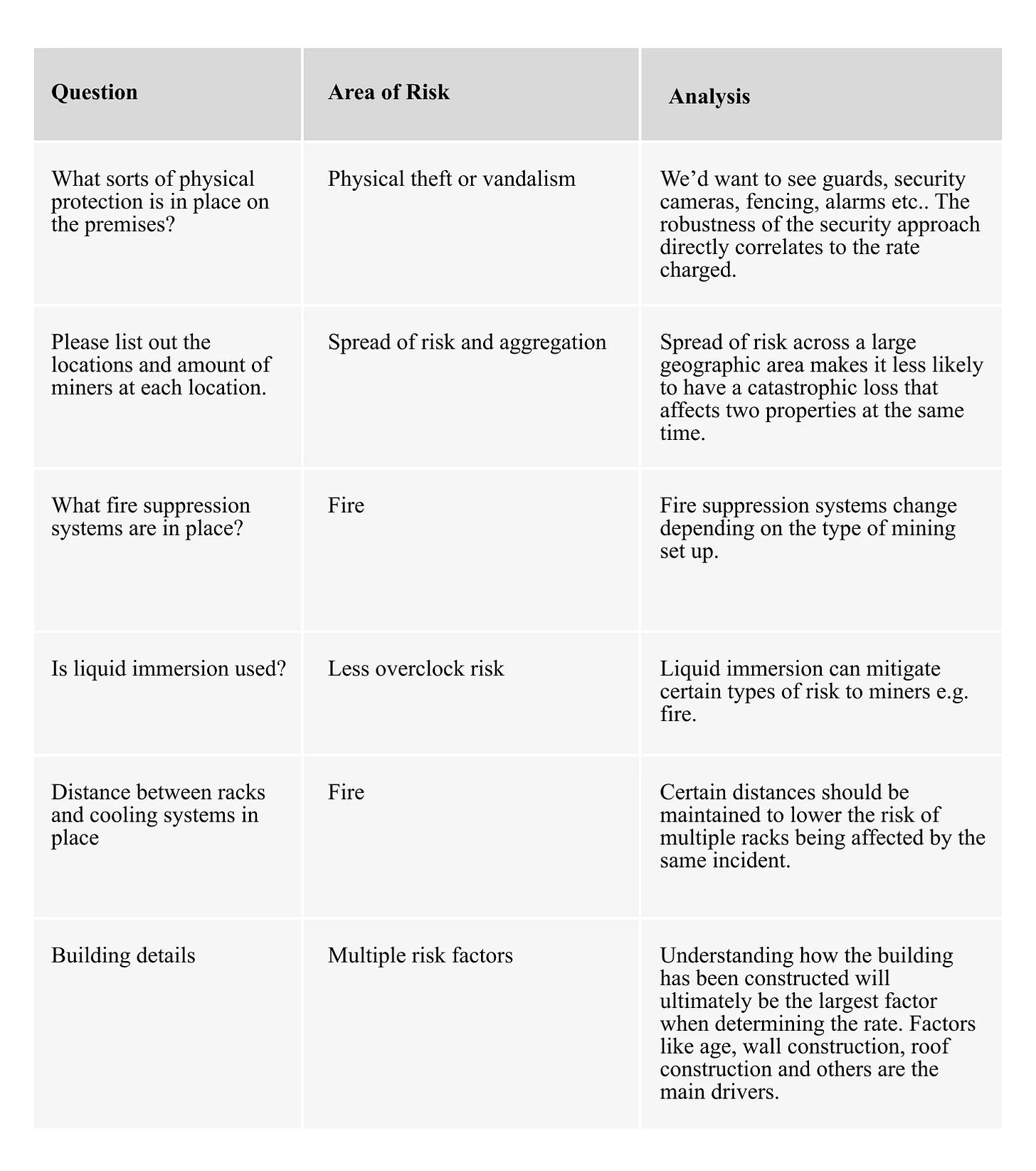

Miner insurance

Miner insurance is a fascinating area of the insurance industry and is one of the most rapidly growing sector out of the entire digital assets ecosystem. Mining insurance protects Bitcoin miners against physical loss of their miners, this could be from fire, flood, earthquake, theft, lightning and hurricane or windstorm. As the value of Bitcoin increases, so does the need for miners to offset their risk onto a balance sheet to enable effective use of their funds and free up operating cash flow.

Here is a non-exhaustive look at what underwriting questions could be asked when assessing mining infrastructure risk:

As seen in the three examples, the underwriting employed is diverse depending on what types of risk is being transferred to the insurer. Although all three risks are different (cyber, physical and liability), we believe that asking some questions from other lines of coverage can enhance the underwriting of another. For example:

- Understanding the financial health of the company can lower cyber risk. If the company is healthy, they are more likely to spend money on cyber risk management and mitigation.

- If the company has robust cybersecurity frameworks in place, there is less of a chance for attackers to compromise the physical security around a mining location that could be used in a multi-step attack.

- If the company has invested in physical security and proper building practices, the directors and officers are less likely to be held liable should an attacker succeed in stealing valuable computing hardware.

So although each of these covers are distinct, a good underwriter takes into consideration other factors that are outside of their typical underwriting framework. Having a holistic approach to the risk enables the underwriter to charge the appropriate rate and for the client to get the right coverage, tailored to their needs.

We’ve taken a look at the risk analysis that an underwriter would do for a risk in the digital asset industry. But what would a day in the life of an underwriter look like?

A Day in the Life of an Underwriter:

Underwriters typically start their day with a mix of underwriting new and renewal accounts. New accounts will be sent to them from brokers and the risk will be their specific area of expertise (D&O, Professional Indemnity, Cyber, Crime etc.). Underwriters will prioritise the urgent accounts that need terms for a deadline or high value accounts. Underwriters can have anywhere from 1 to 30+ accounts to work on in a day (depending on the complexity, size and urgency), in addition to this they also have other tasks:

- Book analysis (business plans, projections and loss ratios)

- Managerial duties

- Mid-term changes on their current accounts

- Client and broker meetings

Most underwriters have a high workload and stringent underwriting authority guidelines that they have to work within. Underwriting authority is the amount of policy limit an underwriter can write without getting approval from their line manager, as well as the class of business. For example, an underwriter could put out a $2m limit without getting approval from their manager, but if the limit is $3m, they then need approval before terms could be released.

For most underwriters, crypto is an excluded class of business from their underwriting authority, due to their ultimate capacity provider or treaty reinsurance restrictions. This means that if a business with crypto exposure comes across their desk they’re already anticipating it’s going to be a headache from an approval standpoint which usually means it goes to the bottom of the pile or delayed until they have time. Couple this with a general lack of understanding of the risk and hesitancy around the industry and you start to understand why insuring digital assets has lagged behind every other tech industry in the world today. Underwriters live and die by their loss ratios and if they are nervous about something they tend to avoid it, or will charge a high rate to justify their underwriting. The thinking goes that at least if there’s a claim, they can justify it by the rate that’s being charged, which also is the main reason behind high premiums for crypto businesses.

This hesitancy coupled with internal hurdles are compounded by the broking of the risk into the underwriter. If the underwriter doesn’t get satisfactory responses to their questions or feels the broker doesn’t understand the risk themselves, it can create a very long and often frustrating process. This more often than not leads to a decline from the underwriter who isn’t already comfortable with digital asset risk.

Having a look into what a day looks like underwriting risks in the digital asset industry can help businesses understand how insurance companies look at their risk and what internal pressures they face and have to navigate. It also highlights the importance of going with a broker that truly understands your business in order to guide an otherwise busy underwriter through your application and hopefully, to quote.

Conclusion

The challenge is clear: digital assets create unique intersections of risk that don't fit traditional models. Cyber security affects physical security. Financial health impacts operational risk. Technical expertise influences everything.

The digital asset market needs robust insurance to backstop its risks. Underwriters who are innovating in this space often face internal pressures and knowledge gaps which make it even harder to protect emerging technologies.

Yet change is coming. As institutional adoption grows and regulation clarifies, 2025 looks set to be a breakthrough year. We expect more standardized coverage, increased capacity, and better integration of technical solutions. For institutions entering the space, success will depend on finding partners who understand both traditional insurance and emerging technology.

Want to keep up to date with Circuit? Sign up below

Related Posts

Discover more about Circuit’s latest News and Research

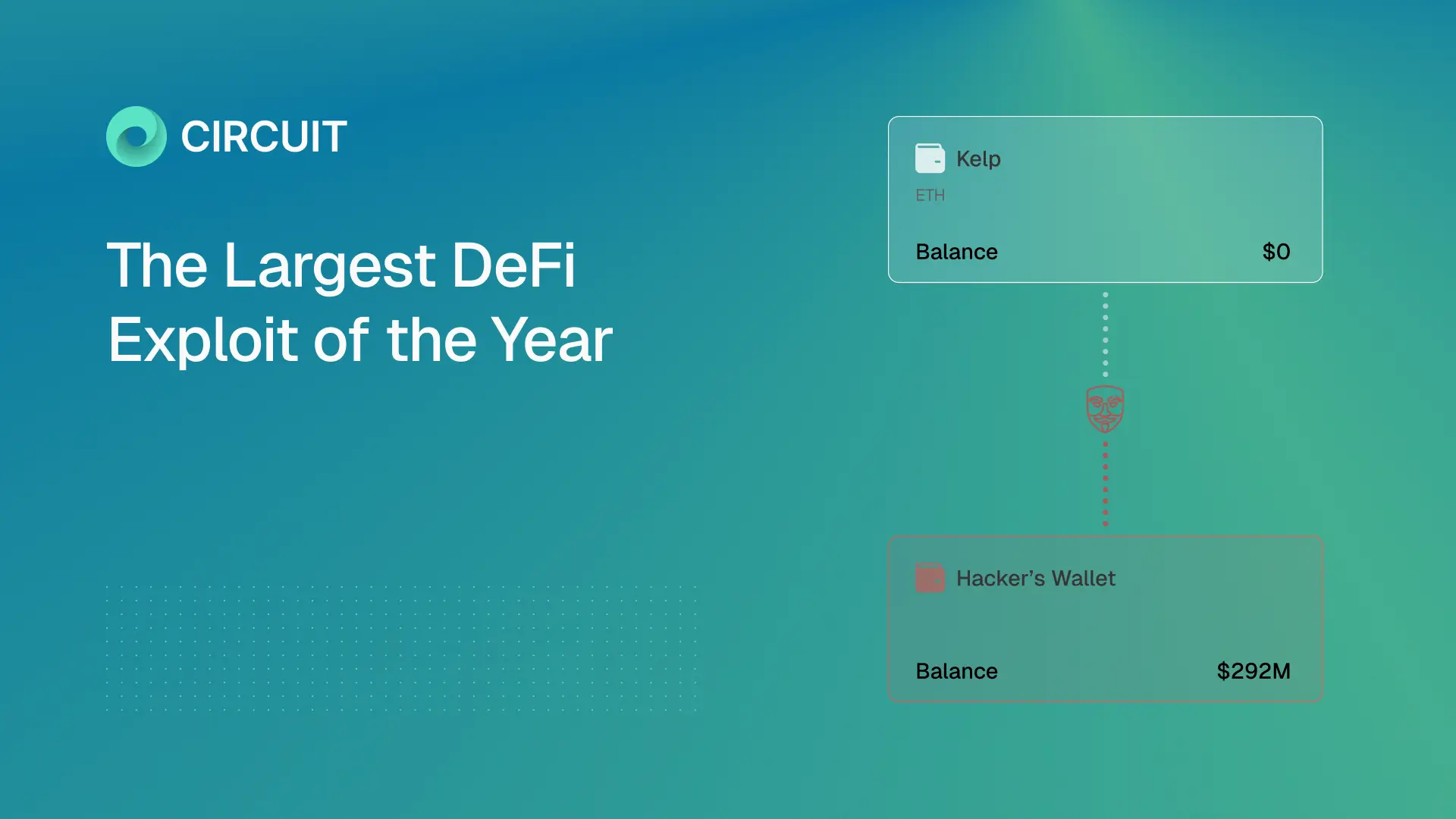

Inside the Kelp/LayerZero Hack: How Lazarus Forged $292M Into Existence

A single lie, six layers deep, and the cascade that pulled in every major lending protocol on Ethereum. A forged cross-chain message led to a $292M exploit draining Kelp and cascading into Aave and DeFi. This breakdown shows how one failure propagated across Ethereum.

$285M Drift Hack Breakdown

A single lie, six layers deep, and the cascade that pulled in every major lending protocol on Ethereum. A $285M DeFi hack executed in 12 minutes after 6 months of social engineering. This breakdown shows how Drift was compromised and what it means for crypto security.

What Google's Quantum Paper Actually Means for Crypto

The largest treasure hunt in human history is already underway. Google’s quantum paper cuts the timeline to break crypto security by ~20x. This guide explains the risks to Bitcoin, Ethereum, and $100B+ in digital assets.

Built by experts who’ve made digital assets safer, and now, recoverable

We believe asset recoverability is table stakes for the next era of digital assets.