Introduction

The biggest hack in crypto history unfolded just weeks ago, $1.4 billion stolen from Bybit in a single attack. Even if they had an insurance policy, it wouldn’t have helped. As institutional money floods in, this gap between digital asset risks and insurance coverage is widening.

This final piece in our 4 part series (read part 1, part 2, part 3 here) examines what's holding the digital asset insurance market back, and where it's headed.

This article examines both current hurdles and future developments. You'll learn:

- The critical technical and regulatory challenges limit market growth

- How new solutions are addressing key problems

- Where institutional demand is driving rapid change

- What the next phase of digital asset insurance could look like

Current Market Challenges

Technical Limitations

While traditional insurers understand physical security and custody risks, most areas beyond that are challenging to assess due to either a lack of historical data or technical knowledge. Many new risks such as smart contract vulnerabilities or slashing don't have perfect parallels in traditional finance or cybersecurity. Without specialized technical knowledge, insurers struggle to evaluate these risks and new solutions emerging to address them.

Limited Historical Data

At its core, insurance is about converting historical data into future risk predictions. Traditional lines of insurance have decades of claims data to analyze. Digital assets present a challenge: limited history, rapidly evolving technology, and new types of risks. Without sufficient data to build accurate actuarial models, insurers either avoid coverage entirely or price in significant uncertainty premiums.

Regulatory Uncertainty

Regulation is becoming both a catalyst and a complication. Hong Kong, Singapore, the EU and Dubai’s VARA require licensed digital asset firms to maintain specific insurance coverage. For multi-jurisdiction firms, these varying mandates create compliance challenges and increase operational complexity. This makes writing global policies challenging.

But the real problem regulation poses is the amount of insurance some regulators require and the available capacity in the market. We touch more on this below.

Capacity Constraints

Combined together, all these challenges create severe capacity limitations. There is only a finite amount of capacity an insurer can underwrite against annually. Once it’s done for the year, they aren’t able to take on any more risk. Traditional insurers remain cautious about deploying significant capital into the digital asset space without better data and risk assessment tools. As a result, capacity remains concentrated among a few providers, particularly for technical risks, leading to high premiums and limited coverage options for institutions.

However, innovation is emerging to address these challenges, and market tailwinds are creating new opportunities for expansion.

Emerging Innovation

New solutions are addressing these core challenges, fundamentally reshaping what's possible in digital asset insurance:

Technology-Enabled Coverage

Innovation is transforming what's insurable in digital assets by shifting from compensation after loss to active prevention.

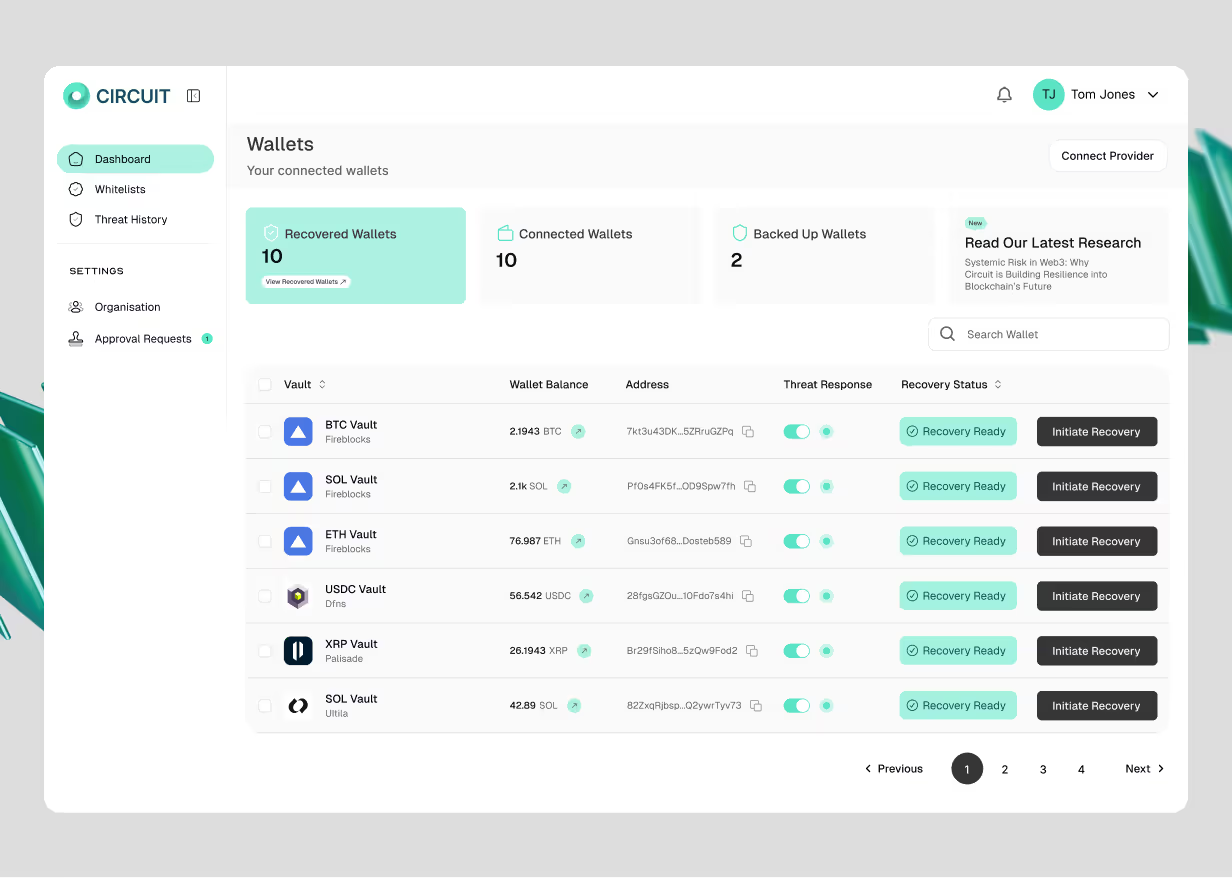

Circuit’s asset extraction technology automatically moves assets from danger to safety without taking custody of the assets. This makes it easier for insurers to underwrite policies like crime coverage because they can actively prevent loss events from occurring. This technology-first approach to insurance will eventually enable real-time, automated coverage adjustments based on actual risk levels. This shift from compensation to prevention represents a fundamental evolution in digital asset insurance.

Hybrid Market Structure

The insurance market itself is evolving beyond traditional models. New capital structures are being built directly on-chain, creating additional capacity through innovative risk-sharing models.

Native is a new insurance broker that understands both traditional insurance and crypto technology, bridging a crucial expertise gap. Hybrid approaches like this, combining traditional insurance expertise with crypto-native technology, are creating more flexible and comprehensive coverage options. For example, Native is able to layer in cover provided by discretionary mutuals like Nexus Mutual into regulated insurance programs, they are also able to create new cover products from scratch with policy limits denominated in digital assets.

Institutional Infrastructure

Institutional adoption is accelerating, with Bitcoin ETFs on track to hold over $100bn in the first year of trading. The institutional infrastructure in place which supports this, from custody solutions to trading platforms, is establishing the standardized risk frameworks that insurers require for efficient underwriting

This clear institutional demand is pushing major carriers who previously avoided the sector entirely to create specialized teams, recognizing digital assets as a permanent addition to the financial landscape. Reinsurance markets are starting to provide additional capacity, helping to reduce premium costs. A virtuous cycle, where increased institutional participation drives better insurance options, which enables further institutional adoption, will start to transform the market.

Looking Forward

Digital asset insurance is poised for rapid evolution over the next few years. These are key trends that are emerging and are worth watching:

1. From Specie to Technology Enabled Crime Coverage

The digital asset custody market is moving from headline insurance numbers to practical risk protection. Currently, custodians choose between two coverage types:

- Specie insurance: Treats digital assets like physical valuables in a vault, covering primarily cold storage with narrow terms but high limits

- Crime insurance: Provides broader protection against theft, fraud and social engineering but with historically lower limits

World renown names have marketed high levels of insurance coverage, sometimes in the range of $1bn. These policies often feature narrow coverage and substantial exclusions, functioning more as marketing tools than comprehensive risk transfer.

We believe this will change as more capital enters into the market. Companies will start demanding that their insurance premiums reflect the safety of their organisations and if not given, will either non-renew or buy lower limits. The most likely outcome will be for custodians to shift to wallet-specific coverage limits rather than maintaining blanket billion-dollar policies. Since no single event typically threatens their entire asset base, properly segregated wallet infrastructure enables more efficient, targeted insurance aligned with actual exposure

The coverage would also broaden to be more akin to crime to cover wallets connected to the internet. Embedding preventative technology will enable insurers to confidently offer this expanded coverage at lower premiums. This will create a more efficient solution that better reflects actual risk while still providing marketing value.

2. Real-Time, Usage-Based Insurance Models

The first wave of "blockchain in insurance" initiatives from 2017 is effectively dead. Those efforts failed because they focused primarily on transitioning insurance company operations to blockchain technology without delivering tangible benefits to end users.

The fundamental insight remains valid: distributed ledgers can transform insurance, but only if they provide what customers actually care about: better coverage, lower prices, or improved service, not just backend efficiency for insurers.

The true opportunity lies in creating entirely new business models that blockchain rails can unlock. As an example, insurers could now offer something unprecedented: real-time, usage-based insurance for digital assets.

Imagine "streaming insurance" that protects hot wallets only during the minutes assets are actually at risk. A trading firm could activate coverage the moment assets enter a high-risk environment and deactivate it when they move to cold storage. If assets are compromised during that window, the policy pays out automatically. This approach aligns cost directly with exposure and could reduce premiums dramatically compared to traditional annual policies.

These models represent a fundamental shift from time-based to activity-based coverage, similar to how streaming transformed entertainment from cable packages to pay-for-what-you-watch.

3. Balance Sheet Innovations

A structural innovation is emerging in how insurers manage their capital reserves. New providers like Soter and Tabit are building balance sheets denominated in Bitcoin, creating a powerful hedge against inflation.

This strategy mirrors what we've seen with public companies like MicroStrategy and Tesla adding Bitcoin to their treasuries. For the insurance industry specifically, this innovation addresses a core business challenge, the eroding purchasing power of premium reserves held in fiat currencies over the multi-year lifecycle of policies. We believe other insurers will start following suit.

4. The Convergence of Traditional and Decentralized Insurance

DeFi insurance (which isn’t technically insurance but discretionary cover) started out with ex-insurance professionals replicating an insurance company with smart contracts. Several companies have tried their hand at this, unfortunately, most have not survived past two years. This is for a number of reasons:

- Distribution. Many of these startups didn’t understand insurance distribution. Most people hate buying insurance, which means it must be sold rather than bought. The fundamental principle of insurance; ‘the claims of the few are paid by the many’ must have the many to pay for the few. Without the many, the insurance provider goes bust. With established players in the space hoovering up the vast majority of the market, the smaller players couldn’t get to the critical threshold needed to support the business model.

- Lack of Aggregation. Coverage was sold without understanding the impact of what one industry wide event could have on multiple clients. When the Terra Luna crash occurred, this one event wiped out a number of smaller providers which sold depeg insurance for Terra Luna.

- Pricing Issues. These startups have historically been limited to onchain cover (depegs, slashing and smart contract risk), which is not easy to price given a lack of data. Coverage was sold cheap which didn’t protect the startup’s capital pool in the event of claims.

- Difficulty. The insurance business model is harder than people give it credit for!

It’s important to analyse the early failures of these pioneers to understand what’s to come, because the market is now entering a second phase which will be where the game really changes.

In phase two, players with experience in traditional insurance will come in to bridge the gap. These insurers will operate smart contracts and regulated balance sheets to instantly bridge capital requirements. This would be as simple as a Lloyd’s underwriter switching her stamp from syndicate to company paper. Phase two will blur the lines between old and new and, we think, will be the upcoming challengers of the established incumbents.

5. Beyond Human Markets: AI as the Next Insurance Frontier

A longer-term opportunity is emerging that could dwarf today's market: autonomous AI agents as insurance customers.

As AI systems become increasingly sophisticated, they're already beginning to interact with blockchain networks. AI agents today can deploy smart contracts, manage digital wallets, and execute transactions with limited human oversight. The next logical evolution will be AI systems that autonomously manage digital assets, enter into contracts of their own volition, and require protection against operational risks.

Traditional financial infrastructure isn't designed for non-human economic actors, but blockchain networks inherently are. Their permissionless nature, programmable smart contracts, and ability to interact without human intermediaries make them the natural foundation for AI financial services.

By building on blockchain rails you’re not only building for the human population of today but for the millions of sentient AIs that need risk transfer solutions in the future. This could quite possibly be the biggest insurance opportunity ever.

Conclusion: The Future of Insurance

Over this series, we've traced insurance from ancient merchants, to today's digital asset landscape, to its future frontiers. Let’s quickly recap:

Where We Started (Part 1)

The intersection of traditional finance and cyber insurance created something new. Early digital asset coverage focused mainly on physical security, treating cold storage like gold in a vault. But the industry needed more.

The industry evolved to incorporate smart contracts, blockchain and digital assets into risk transference to provide businesses a more fit for purpose product for managing these emerging threats.

Where We Are (Part 2)

Today's market shows stark contrasts. Some risks, like cold storage, attract hundreds of millions in coverage at reasonable rates. Others, like smart contracts, remain challenging to insure at any price. The market is fragmented, with capacity concentrated among few providers.

What's Changing

Several forces are reshaping the landscape:

- Institutional adoption driving demand for comprehensive coverage

- Regulatory frameworks creating clear operating environments

- New technology enabling previously uninsurable risks

- Traditional insurers building crypto expertise and balance sheets

- Innovative capital structures expanding capacity

What's Next

2025 looks set to be a breakthrough year. As standardization increases, capacity expands, and technology becomes embedded in coverage, we expect:

- More standardized policy terms

- Lower premiums as competition increases

- Technology risk mitigation providers becoming a requirement for coverage

For institutions entering digital assets, the message is clear: insurance is evolving from a barrier to an enabler. Those who understand both traditional frameworks and emerging solutions will be best positioned to protect their assets in this new frontier.

If you're looking to better understand your digital asset insurance options or how new technology can help protect your assets, reach out to Circuit or Native to learn more.

Want to keep up to date with Circuit? Sign up below

Related Posts

Discover more about Circuit’s latest News and Research

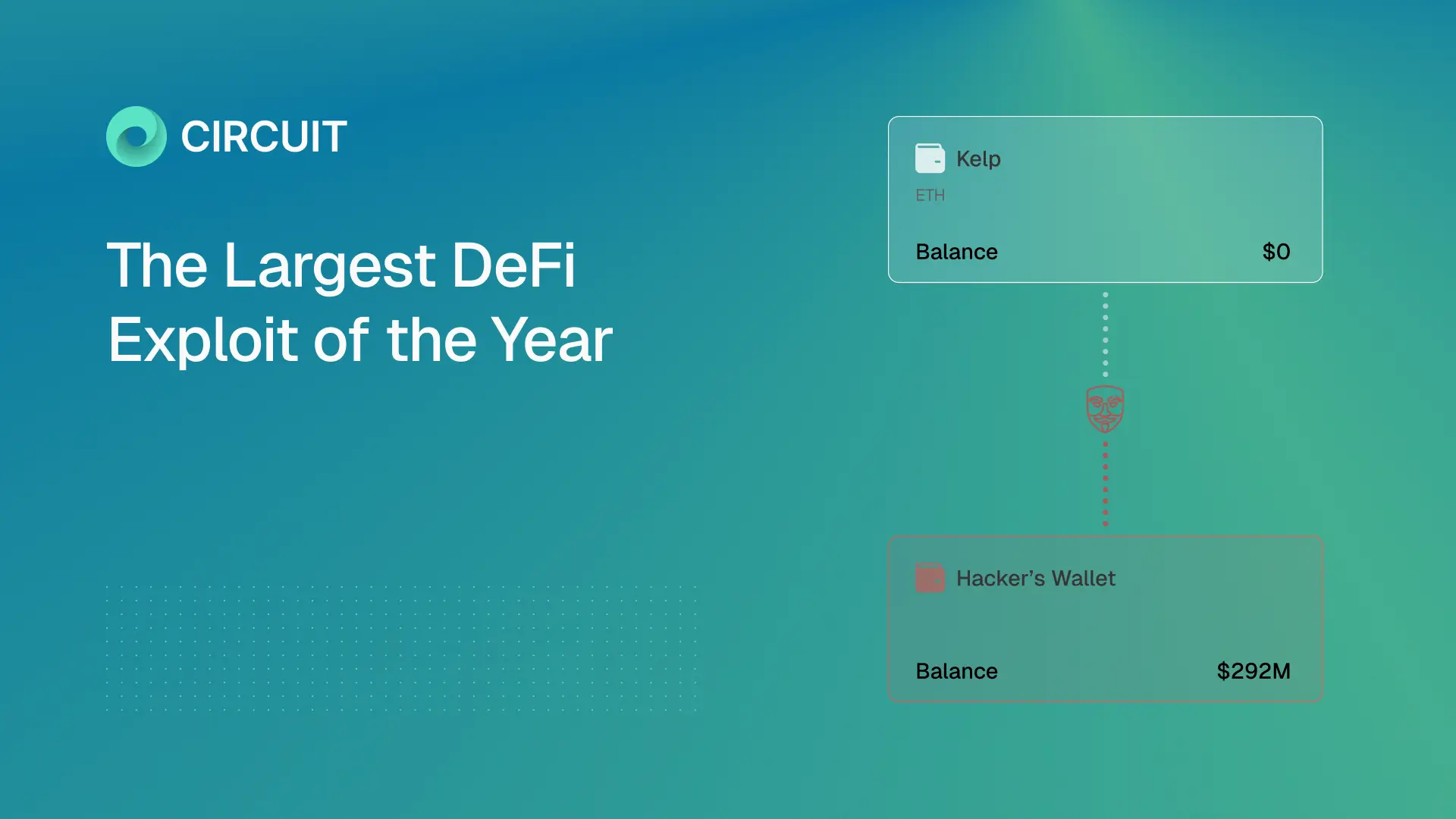

Inside the Kelp/LayerZero Hack: How Lazarus Forged $292M Into Existence

A single lie, six layers deep, and the cascade that pulled in every major lending protocol on Ethereum. A forged cross-chain message led to a $292M exploit draining Kelp and cascading into Aave and DeFi. This breakdown shows how one failure propagated across Ethereum.

$285M Drift Hack Breakdown

A single lie, six layers deep, and the cascade that pulled in every major lending protocol on Ethereum. A $285M DeFi hack executed in 12 minutes after 6 months of social engineering. This breakdown shows how Drift was compromised and what it means for crypto security.

What Google's Quantum Paper Actually Means for Crypto

The largest treasure hunt in human history is already underway. Google’s quantum paper cuts the timeline to break crypto security by ~20x. This guide explains the risks to Bitcoin, Ethereum, and $100B+ in digital assets.

Built by experts who’ve made digital assets safer, and now, recoverable

We believe asset recoverability is table stakes for the next era of digital assets.